Value Judgment

A 2018 Texas Supreme Court decision regarding the Texas Property Tax Code could open the door for legislative measures aimed at favoring particular categories of owners and undermining the integrity of the property tax base. However, it might also solve some long-standing problems involving complex properties, such as those related to transportation and infrastructure. |

Every year when property values are reassessed, thousands of Texans face off with their central appraisal districts hoping to obtain the lowest property value possible and avoid a large tax hike. Some observers worry that a 2018 Texas Supreme Court decision could give property owners new cause for concern by opening the door for measures aimed at favoring particular categories of owners and undermining the integrity of the property tax base.

The Texas Property Tax Code creates the legal framework that guides property value disagreements to conclusions conforming to requirements found in Article VIII, Section 1 of the Texas Constitution. Granting the right to tax, this section of the Constitution immediately specifies:

- Taxation shall be equal and uniform.

- All real property and tangible personal property . . . shall be taxed in proportion to its value, which shall be ascertained as may be provided by law.

In addition, Article VIII, Section 20 of the Constitution provides, in part, that “no property of any kind in this State shall ever be assessed for ad valorem taxes at a greater value than its fair cash market value, nor shall any Board of Equalization of any governmental or political subdivision or taxing district within this State fix the value of any property for tax purposes at more than its fair cash market value . . ."

Those provisions have caused most property tax disputes to focus on the classic notion of market value, loosely defined as the most probable price that a willing buyer would pay a willing seller.

The Texas Legislature has passed laws specifying specific formulas for calculating taxable value for various kinds of property. Article VIII, Section 1-d of the Constitution requires that qualifying agricultural land be appraised at its productivity value. Article VIII, Section 1(i) authorizes a value limitation for residence homesteads that is codified in Section 23.23 of the Property Tax Code. The law limits the increase in appraised value of qualifying residence homesteads to 10 percent from the last reappraisal. These provisions specify values other than traditional market value for determining tax liability but only with constitutional authorization.

Another Tax Code provision (Section 23.1241) applies to setting the value of a dealer’s heavy equipment inventory. This section recognizes the difference between the value of items held in stock for sale (inventory) and their individual values when sold to a user. It also provides the valuations method to apply when appraising both inventory held for sale and inventory leased to others. For leased heavy equipment inventory, the specified value equals the total annual rental payments divided by 12 (Section 23.1241[b]).

New Property Tax Policy Precedent

EXLP Leasing LLC (EXLP) owned a compressor it held as inventory and leased to a company in Galveston County. Contending the compressor did not qualify as heavy equipment inventory, the Galveston Central Appraisal District (District) denied the declaration for the special appraisal and treated the item as taxable business personal property. The District determined a taxable value based on a comparable sale price for the compressor. EXLP objected, contending the machine qualified as heavy equipment inventory under Section 23.1241 because a heavy equipment dealer owned it and met the other definitions and qualifications in law. The District disagreed, and the fight was on.

Eventually, the case moved to the Texas Supreme Court. The District argued that Tax Code Section 23.1241 violated the Constitution. Further, it contended that compressors do not meet the definition of “heavy equipment." EXLP replied that the legislature has the authority to prescribe a method to value compressors, the compressors are heavy equipment, and Washington County should tax the compressor because the dealership that owned the compressor was located there. The District prevailed in lower courts but failed in the Supreme Court on the issues of taxable situs and the constitutionality of the statutory appraisal methodology.

In its legal arguments, the District argued that the formulaic value in the Tax Code strayed from the market value principles of “willing buyer-willing seller" and produced a result much lower than a sales price of a compressor. Only by considering sales, argued the District, could the appraisal of the leased inventory properly correspond with the definition of market value in the Texas Constitution and Tax Code Section 1.04(7). The District contended market value appraisal constituted the proper valuation method required by the Constitution. Because past Supreme Court decisions in property tax cases referred to “market value" when interpreting Article VIII, Section 1(b), the District contended those decisions recognized market value as the constitutional standard.

Weighing these arguments, the Supreme Court pointed out that Article VIII, Section 1(b) refers only to “value," not “market value." In addition, that section also grants the legislature the authority to provide laws specifying how to determine taxable value. The language does not specifically say “market value." In addition, market value as used in the Texas Property Tax Code merely represents “a catch-all reference to taxable value produced through application of the code’s rules," according to the Supreme Court.

The opinion stated that the cases cited by the District did not enshrine market value as the overall standard for property taxation. The District did not assert that Section 23.1241 amounted to an “unreasonable, arbitrary, or capricious" scheme of taxation. Instead, the District contended that the resultant value was unfair. The Supreme Court deferred to the legislature to set the standards of fairness.

The Supreme Court decided that the statutory appraisal methodology for heavy equipment inventory is constitutional, a leased compressor was part of the heavy equipment inventory of the owner under the facts of the case, and Washington County was the proper situs for taxation. This sweeping result empowers the Texas Legislature to specify methods to calculate value for property tax purposes without seeking constitutional amendments.

The District also argued that the Section 23.1241 appraisal methodology deviated from the market value standard leading to a violation of the equal-and-uniform provision of Texas Constitution Article VIII, Section 1(a). Because other properties paid taxes based on the classical definition of market value, this leased inventory value resulted in unequal taxation. The inventory taxation discriminated against those persons or companies owning their own compressors, the District contended. However, the Supreme Court noted that prior decisions allowed the legislature to distinguish between properties, and the equal-and-uniform provision “generally applies only within classes of property, not between classes." This notation implies that the legislature can authorize the appraisal of different categories of property differently without transgressing constitutional requirements.

This decision will require local taxing units to refund taxes for the years the property was not appraised as heavy equipment inventory. In addition, other counties had applied the same arguments and also were sued. Now taxing units in those counties will face a demand for refunds as well.

Besides creating fiscal problems for taxing units, this decision amounts to a revolution in Texas property tax policy and litigation. In the past, departures from recognized methods of estimating market value had to pass muster with the Texas electorate to become official parts of the Constitution. From now on, the legislature can adopt measures targeted to specific classes of property without a constitutional amendment.

Implications for Railroad, Pipeline, and Public Utility Properties

While the legislature faces new opportunities that could pose problems in the future, those newfound powers might help solve some long-standing problems. For example, the task of appraising railroad, pipeline, and public utility properties has sparked controversy for more than a century. Is the value of railroad tracks through a taxing unit equal to the current value of the land plus the cost of adding the rails, or is it the value it contributes to the operation of the railroad? Many states value the railroad as an operating unit and apportion the resulting value to the local transportation corridor.

Ultimately, no specific techniques can credibly claim to result in a value that fits the definition of market value in a strict sense. However, officials everywhere have argued that their approach correctly produced such a result.

In Texas, each chief appraiser must value this kind of asset for the taxing units in the counties. They often hire expert appraisal firms to develop the values for them. The Texas Property Tax Code does not currently specify a method to develop taxable values for railroad, pipelines, and public utility properties. Most appraisers probably rely on some form of unit appraisal to establish values for this kind of property. Because conventional wisdom presumed the result had to produce a “market value," both taxpayers and taxing jurisdictions insisted they knew the proper method to achieve that end.

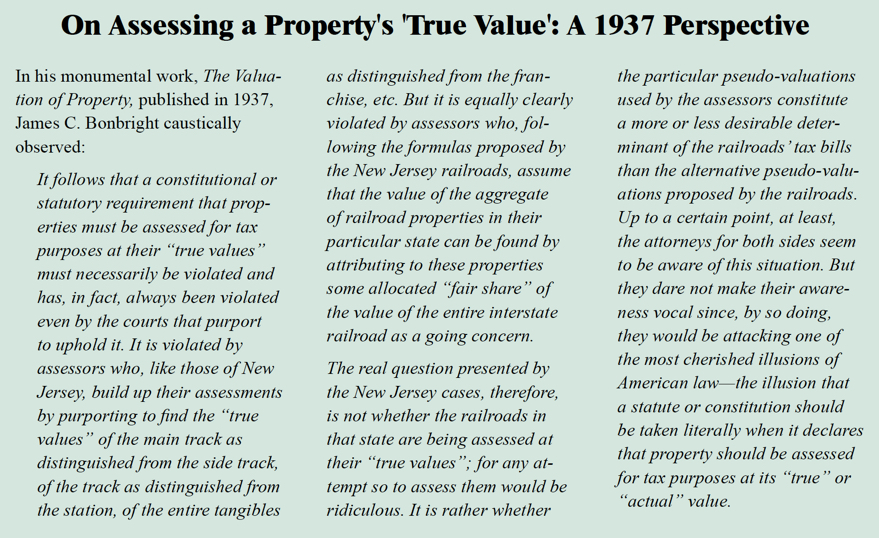

Forty odd years after publishing

The Valuation of Property (see sidebar), James C. Bonbright, commenting on New Jersey tax controversies, observed:

Our problem is that of finding a reasonable allocation of value, and we must make it reasonable, not because it is defining a value of the New Jersey portion, but it has to be reasonable for some other reason . . .

The

EXLP Leasing Inc. v. Galveston Central Appraisal District decision gives the Texas Legislature the authority to specify how to determine a reasonable taxable value for any category of property. Perhaps the decision will lead the legislature to eliminate some of the controversy prevalent in the system today regarding complex properties such as railroads, pipelines, and public utilities.

____________________

Dr. Gilliland ([email protected]) is a research economist with the Real Estate Center at Texas A&M University.

You might also like

TG Magazine

Check out the latest issue of our flagship publication.