Losses and Self-Employment Taxes

Owners of profitable income-producing real estate cannot offset their net income by unrelated business losses of a spouse when computing self-employment (SE) taxes. This rule was underscored by a 2013 tax court case and is even more relevant today because SE tax rates increased since the transactions in the court case.

Owners of profitable income-producing real estate cannot offset their net income by unrelated business losses of a spouse when computing self-employment (SE) taxes. This rule was underscored by a 2013 tax court case and is even more relevant today because SE tax rates increased since the transactions in the court case.

The 2013 case pertains to Brenda and Donald Fitch, who resided in California during the period of the contested tax filings. Note that both California and Texas are community-property states. SE taxes are applied in the same manner in all 50 states in virtually all instances. Brenda was a licensed real estate agent under California law and a member of the National Association of Realtors. Donald, a CPA, owned and operated a CPA practice. He spent four hours per day working at his practice. (He was recovering from a medical condition.)

Apart from their respective Realtor and CPA businesses, the couple owned and managed eight rental properties. They chose to own their properties separately. Brenda owned three of the properties. Donald owned five. They each performed day-to-day tasks related to their respective rental properties. Donald occasionally helped Brenda with advertising and repairs.

During the three years in question, the taxable income associated with Brenda’s properties ranged from $2,000 to $21,000. In contrast, Donald’s CPA practice generated losses ranging from $59,000 to $69,000 during the same period. The couple reduced Brenda’s taxable rental income to zero by offsetting her income by Donald’s losses. This approach was determined to be acceptable for income tax purposes but not for SE tax purposes.

In addition to back taxes and interest, the Fitches were assessed accuracy penalties from $67 to $584 for the years in question. The court determined that the penalties were appropriate due to the Fitches’ "intentional disregard" for SE tax rules.

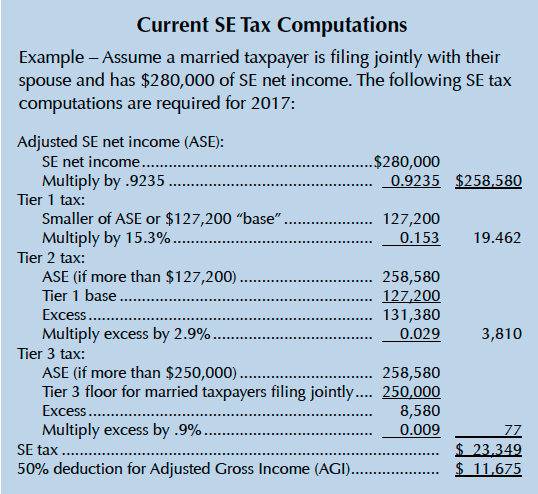

While the dollar amounts in this case are not large, the manner in which the SE tax rules and penalties were applied is the major concern. In addition, SE tax rates have increased since 2013 (see example).

The example illustrates (1) the SE tax base amount for 2017 is $127,200 (increased annually for inflation); (2) there are up to three tiers of tax depending on the size of the taxpayer’s SE income; (3) while there is a limit for the Tier 1 tax, there is no limit for the Tier 2 or Tier 3 taxes, which are intended for high-income taxpayers; and (4) one-half of the SE tax can be deducted when computing adjusted gross income (AGI).

As discussed and shown here, SE tax issues can be complex from both a rules and computation perspective. Consultation with an accountant or attorney knowledgeable about real estate tax matters is recommended.

____________________

Dr. Stern ([email protected]) is a research fellow with the Real Estate Center at Texas A&M University and a professor emeritus of accounting in the Kelley School of Business – Bloomington, at Indiana University.

You might also like

TG Magazine

Check out the latest issue of our flagship publication.