Highs and Lows of Floodplain Regulations

Houston’s revisions to its floodplain ordinance could diminish housing affordability in the short term by increasing construction costs and, therefore, home prices. In the long run, the benefits incurred from mitigating flood damage may outweigh the increased construction costs. |

Houston, the nation’s fourth-largest city and home to a burgeoning oil and gas sector, has weathered three major flooding events over the past three years: the Memorial Day Flood of 2015, the Tax Day Flood of 2016, and Hurricane Harvey in 2017. Concerns over the capacity of the city’s infrastructure to sustain severe flooding have mounted as thousands of households have faced massive rebuilding efforts in the wake of the natural disasters. A total of around 200,000 owner-occupied households in Harris County have registered for Federal Emergency Management Agency (FEMA) assistance because of these events, disrupting both the housing market and the broader economy.

As a result of the flood events, the city and Harris County have revised construction requirements. While revisions to the city’s floodplain ordinance promise to reduce residential damage from flooding events, they may negatively impact housing affordability by lengthening the time and increasing the cost of new-home construction. This will raise the price of new homes within the floodplains. However, the ordinance could mitigate housing damage and loss from flooding, thereby reducing the shock on home prices in the wake of flooding.

Floodplain Ordinance Revisions

Houston’s city council approved revisions to its floodplain ordinance in April 2018. The revisions, which were implemented September 1, 2018, will require new homes constructed in the 500-year floodplain to meet a minimum elevation at the 500-year floodplain plus two feet. Previously, the ordinance applied only to the 100-year floodplain and required a minimum elevation at the 100-year floodplain plus one foot. According to attorney Omar Izfar and professional engineer James Jones, “the revisions [to the floodplain ordinance] add an additional 51,200 acres (13 percent of the overall city limits) to the area regulated by floodplain ordinance."

The revisions apply primarily to new-home construction, but they also affect the owners of existing homes who build an addition or improve the home’s structure at a cost of more than 50 percent of the value of the existing improvements. Other owners of existing homes are not required to elevate their property, but they may be subject to increased home insurance cost or they may lose access to flood insurance. The revisions apply only to the incorporated areas of the City of Houston, but outlying areas may adopt the revisions in the future.

Effect of Natural Disasters on Housing Affordability

The impact of natural disasters on housing affordability greatly depends on the health of the region’s economy and housing market. FEMA reported a total of $1.04 billion in residential damage from Hurricane Harvey in Harris County and approved 87,316 owner-occupied households in the county for assistance, representing approximately 10 percent of all owner-occupied households. Homeowners whose properties were left uninhabitable faced several options:

- seek temporary housing and rebuild the home,

- sell the home and purchase a different home or rent a housing unit in Houston,

- sell the home and leave Houston.

The first and second option would accelerate the demand for housing units in the region.

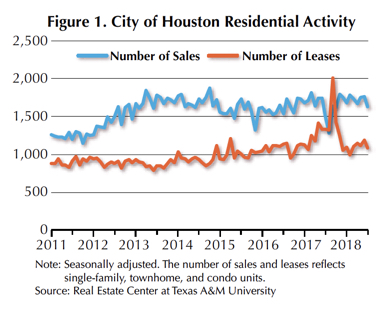

In the short run, the supply of undamaged housing units declined after Hurricane Harvey. Meanwhile, the demand for units increased as households that sustained property damage sought temporary housing. New residential leases spiked in Houston in September 2017, more than doubling those of the prior year, indicating strong household demand for temporary housing (Figure 1). The shock pushed the median rent of new residential leases up nearly 10 percent year over year in September 2017. Rising rents contributed to the disproportionate impact of Harvey on lower-income households.

Following Harvey, two opposing forces—an increase in demand for housing units and a decrease in supply of undamaged housing units—reduced housing affordability in Houston. Harvey particularly limited the supply of homes affordable to lower-income households as the hurricane disparately damaged lower-income regions in the city (for more on this, read “Imperfect Storm" at www.recenter.tamu.edu).

In the long run, demand shock for housing units will taper as households with damaged homes relocate to permanent housing. As the rebuilding process progresses, Houston’s housing stock will return to levels observed prior to Harvey. Housing affordability should improve but may not reach its pre-Harvey status as new construction or remodeling raises the price of a home.

Most Impacted Areas

The highest proportion of housing damage occurred northeast of downtown in economically disadvantaged neighborhoods. These areas consist primarily of older, smaller, and lower-priced existing homes, suggesting new building regulations may have more impact on the most vulnerable areas (Table 1). Residents in these regions may face increasing difficulty in financing housing modifications, such as elevating homes to comply with proposed building codes. Additionally, rapid home price appreciation heightens financial burdens for these residents as rising property taxes further strain disposable income levels.

The demographic characteristics of the ZIP codes with the highest proportion of housing damage indicate residents are of lower income and a higher percentage live below the poverty level (Table 2). These neighborhoods contain a higher proportion of minorities than the city; residents are also generally less educated. Exceptions to these demographic trends are in the 77044, 77089, 77050, and 77079 ZIP codes.

Floodplain Ordinance and Housing Affordability

Floodplain ordinance revisions may reduce Houston’s housing affordability by increasing the cost of new residential construction. However, by mitigating adverse structural damage from natural disasters, the revisions should prevent a negative shock to the supply of undamaged homes following flooding. This will reduce the effects of flooding on housing affordability.

The cost of elevating a new home varies depending on the size of the home and the type of foundation. According to Metrostudy, elevating a slab by one foot adds approximately $35,000 to the construction cost (this includes decking and railing). Each additional foot of elevation increases the cost of the slab by $10,000. Therefore, the cost of elevating a new home by two feet is $45,000; by three feet, $55,000, and so forth. The cost of elevation decreases (increases) as the size of the home decreases (increases).

For existing homes, the cost of elevation is actually higher due to the greater intensity and difficulty of labor involved. According to the architectural firm Arkitektura Development, elevating an existing home costs an estimated $75 per square foot. The median size of an existing, single-family, for-sale residence in Houston was 2,168 square feet as of March 2018. The cost of elevating a home this size is $162,600.

The cost of elevating a home will significantly impact housing affordability for lower-income households. Each incremental increase in the cost of elevating a home reduces the already constrained supply of homes that are affordable to lower-income households. As a result, the price of homes, particularly lower-priced homes, will increase.

Quantifying the Effect of Floodplain Revisions on Housing Affordability

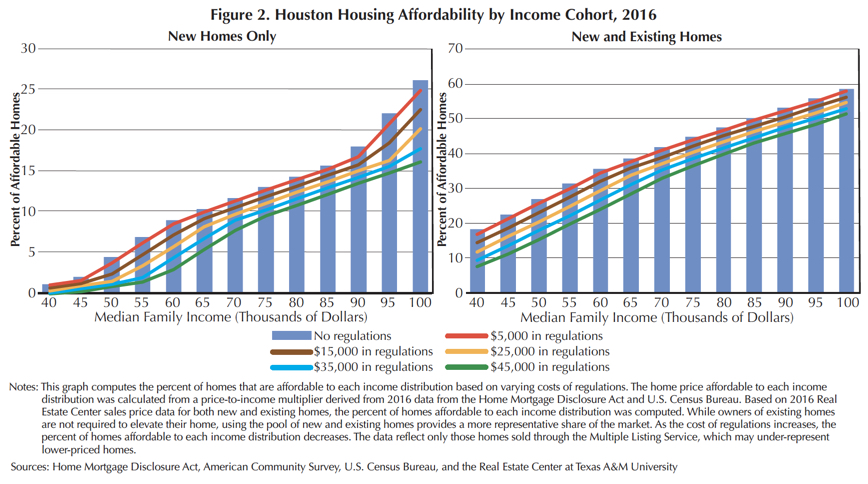

The Real Estate Center calculated the effect of the revisions on Houston housing affordability. The analysis computes the percentage of homes that are affordable to each income distribution based on different costs of elevation. It assumes that the purchase price of a new home increases in proportion to the cost of elevating the home (i.e., the homebuilder passes all costs of elevating the home onto the buyer). The analysis calculates the affordability impact on both new and existing homes in $10,000 intervals.

The home price that is affordable to each income distribution figure was calculated from a price-to-income multiplier derived from the Home Mortgage Disclosure Act (HMDA) 2016 data, U.S. Census Bureau, and the Center (2017 data from HMDA and the Census Bureau have not been released). The analysis calculates affordability for two measures of housing supply: new single-family homes for sale and both new and existing single-family homes for sale. Because the revisions apply primarily to new single-family homes, it is important to isolate the effect of the revisions on new-home affordability. However, as the supply of new homes represents a small portion of the total stock, using the pool of both new and existing homes provides a more representative share of the market. Furthermore, the rising price of new homes in response to the cost of elevating a home may induce upward pressure on the price of existing homes.

In 2016, a family with a $50,000 income could afford a $170,207 home. Barring any regulations, only 4.5 percent of new single-family homes for sale in Houston were affordable at this income level. As the cost from regulations increases, that percentage drops (Figure 2). If the cost of elevating a new home in Houston averaged $25,000, 1.5 percent of new single-family homes would be affordable to households that earned $50,000. However, because not every new home lies in a floodplain, this percentage underestimates the stock of new homes affordable to these households. A mere 0.8 percent would be affordable to those households if the cost of elevating a home averaged $45,000.

Housing affordability improves when accounting for existing single-family homes for sale (Figure 2). Without any regulations, 27.0 percent of new and existing single-family homes for sale in Houston would be affordable to households earning $50,000 in 2016. If the cost of elevating the home averaged $25,000 across the city, 20.5 percent would be affordable to these households. The proportion of affordable homes would decline to 15.4 percent if the cost of elevating a home averaged $45,000.

In some

ZIP codes, the cost of elevating a home may actually exceed the median home price. For example, the median home price for the ZIP code with the highest proportion of home damage (77078) is $78,200 (Table 1). The median square footage of a home in this area is 1,371 square feet, and the cost of elevating a home this size by one foot is $102,825. Thus, the cost of elevating a home outweighs the median price by nearly $25,000. Based on the median household income and age of homes in this ZIP code, elevating the home is economically unfeasible. An additional financial headwind would be the cost of temporary living while the new home is under construction or being elevated.

The revisions to the floodplain ordinance will increase the cost of new-home construction, which will likely erode housing affordability. Housing affordability for lower-income households, which experienced more housing damage, will be disproportionally impacted. However, the long-term benefits (e.g., lives and private property saved) of alleviating the physical vulnerability of homes to flooding may outweigh the increased construction costs although most research has found that the costs of regulation outweigh the benefits by a substantial margin. It will take time to see how homebuilders and buyers respond to the new regulations.

____________________

Dr. Torres ([email protected]) is a research economist, Losey a research intern, and Miller ([email protected]) a research associate with the Real Estate Center at Texas A&M University.

You might also like

TG Magazine

Check out the latest issue of our flagship publication.