High Anxiety

Inflation diminishes purchase affordability by widening the gap between home price and income and increasing borrowing costs. It diminishes repayment affordability by eroding residual income and hiking the homeowner’s property tax burden. In both instances, the effects will prove most detrimental to low-income and elderly households. |

High home price appreciation emerged as a nationwide trend during the COVID-19 pandemic, with year-over-year (YOY) appreciation hitting double digits in January 2021. It shows little sign of abating anytime soon. Meanwhile, labor shortages, supply chain bottlenecks, and increased consumer spending following the rollout of the COVID-19 vaccine and the return of workers and consumers to offices and businesses have accelerated a rise in the costs of goods and services, prompting inflation.

Although inflation was initially expected to be temporary, revised forecasts indicate it may be more long-term. Inflation has significant implications on the housing market—at least in the short-term, and particularly for low-income buyers. Inflation pushes up home prices, diminishes a household’s purchasing power, and may prompt a rate hike by the Federal Reserve Bank, resulting in marginal increases in the mortgage interest rate. All three factors reduce affordability when it comes to either purchasing a home or repaying a mortgage.

Inflation and Purchase Affordability

Purchase affordability is the ability of a household (whether a renter or existing owner) to buy a home. Inflation affects purchase affordability primarily by widening the gap between home price and household income.

Increases in the costs of goods and services, including construction materials and labor, have caused home prices to rise. The National Association of Home Builders reported that the price of inputs to residential construction jumped 12.3 percent since the beginning of 2021. These price increases are passed on from builders to consumers through higher home prices.

Meanwhile, cost increases reduce people’s purchasing power by making them spend more money on the same product or service, leaving less money for other things.

In addition, inflation can result in higher home price appreciation, which increases home prices and, consequently, how much income a buyer needs to qualify for a mortgage. For example, a $150,000 home would increase slightly to $153,000 after one year of appreciation at 2 percent, but it would rise significantly to $172,500 after one year at 15 percent (Table 1). This makes the required income to qualify for a mortgage loan $49,250 at a home price appreciation rate of 2 percent and $55,527 at a home price appreciation rate of 15 percent (Table 2).

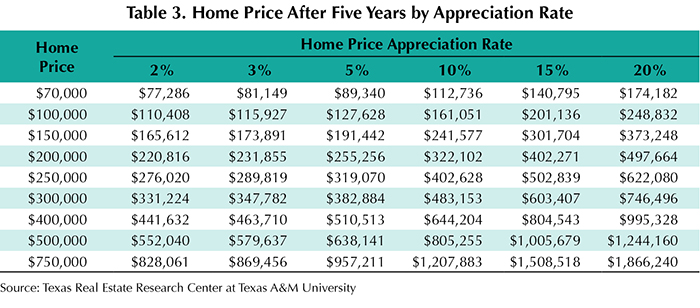

Appreciation takes an even greater toll over time. After five years of appreciation at 2 percent annually, that same $150,000 home would increase to $165,612 (Table 3). At 15 percent, though, the price would more than double to $373,248. This means an income of $53,310 is necessary to qualify for a mortgage at a home price appreciation rate of 2 percent, while an income of $97,117 is needed at a 15 percent appreciation rate (Table 4). Clearly, persistent high home price appreciation decreases purchase affordability. While it is uncommon for a market to have a 15 percent annual home price appreciation rate for five consecutive years, this exercise shows the significant effect of high home price appreciation on purchase affordability.

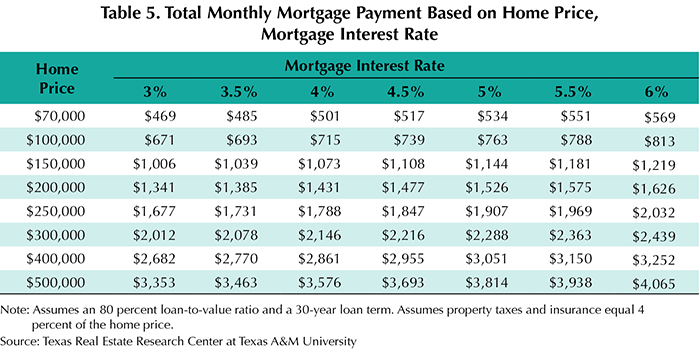

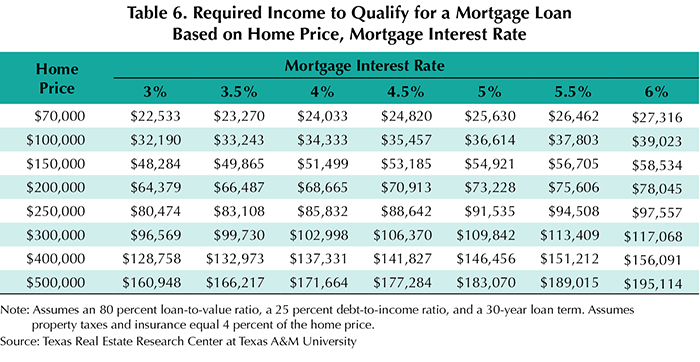

Inflation can also cause mortgage interest rates to increase, affecting the cost of borrowing. As the interest rate increases, the total monthly mortgage payment increases (Table 5), which increases the income required to qualify for a loan (Table 6).

For instance, a buyer who purchases a home for $200,000 can expect a total monthly mortgage payment (principal, interest, property taxes, and insurance) of $1,341 with a 3 percent mortgage interest rate. That increases by nearly $100 per month—$1,431 in total—with a 4 percent rate (given the assumptions stated in Table 6). This raises the income required to qualify for a mortgage loan from $64,379 to $68,665—a nearly 7 percent increase. A rise in mortgage interest rates particularly affects low-income homebuyers.

Inflation and Repayment Affordability

Repayment affordability is a homeowner’s ability to make timely monthly mortgage payments. Inflation affects repayment affordability primarily by eroding residual income.

The more a homeowner spends on basic necessities like food and gas, the less residual income they have. Low-income homeowners and homeowners who lose their jobs likely have even less residual income, making it especially difficult to make timely monthly mortgage payments. Meanwhile, rapid home price appreciation increases appraised values, raising the homeowner’s property tax burden. Although tax exemptions such as the homestead exemption cap the annual increase in property taxes, such increases can still put stress on households over time. This may make homeownership unsustainable for low-income and elderly homeowners (or other homeowners on a fixed income).

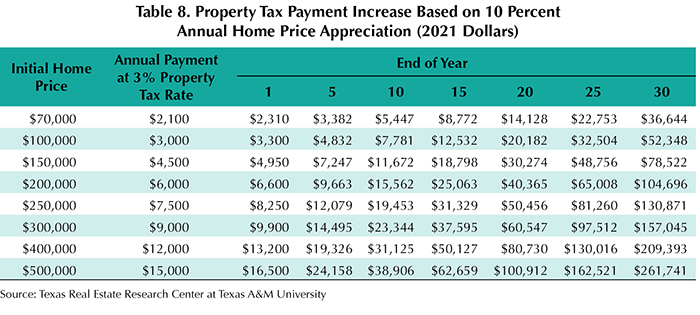

For example, the annual property tax payment for a home purchased for $200,000 is $6,000 at a 3 percent tax rate (Table 7). Should home price appreciation measure 3 percent annually, the tax payment increases to $6,956 in five years and $10,837 in 20 years in 2021 dollars. Should home price appreciation measure 10 percent annually, the property tax payment rises to $9,663 in five years and $40,365 in 20 years, also at a 3 percent tax rate and in 2021 dollars (Table 8).

Such a precipitous increase would significantly strain the average household. Of course, it is highly unlikely any market would witness such high growth over two decades.

Are High Appreciation Rates Here to Stay?

Prior to the COVID-19 pandemic, YOY growth in home price appreciation generally hovered between 3 and 6 percent nationwide. In 2019, it averaged 3.5 percent. Although it rose slightly in 2020, it increased considerably in 2021, measuring nearly 20 percent in July 2021.

This level of growth in home price appreciation is unsustainable in the long-run, and growth will likely dissipate, but it is unlikely that home prices themselves will decline.

Furthermore, the story may bear out differently for Texas than most other states thanks to the state’s strong population growth and increasing demand for homeownership.

____________________

Dr. Losey ([email protected]) is an assistant research economist with the Texas Real Estate Research Center at Texas A&M University.

You might also like

TG Magazine

Check out the latest issue of our flagship publication.