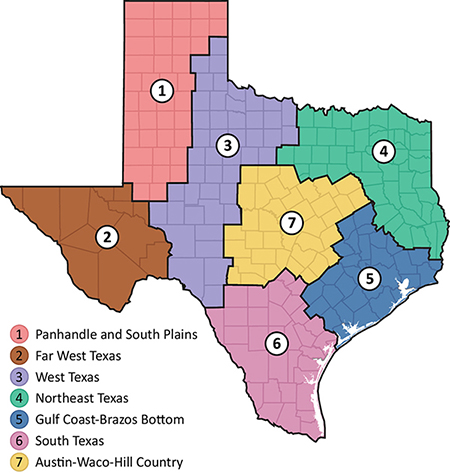

Structural Trends of Regional Texas Rural Land Markets

Various factors impact local land market prices and activity. The size of offered properties has a large influence on the marketing possibilities. Specifically, buyers simply cannot afford properties beyond a certain size. Similarly, they frequently have a particular sum dedicated to the land purchase. They need to find tracts large enough to use all of that dedicated investment. In this manner, most buyers find themselves considering properties within a range of sizes. In a sense then, land markets consist of a series of properties occupying different size-segments of the overall market. Consequently, buyers and sellers compete with similarly situated buyers and sellers.

This segmentation can lead to different dynamics in market trends, especially in challenging times as buyers respond differently to the situation. For example, markets for the largest properties frequently freeze up in times of turmoil. The limited number of buyers in this market anticipate future weakness. They withdraw from the market or make low offers. Sellers greet these offers with disdain, and transactions cease. Meanwhile, the smaller ends of the market involve a larger population of potential buyers, and, although prices may slip, transactions continue.

That scenario emerged in Texas in 2009 in the wake of the Great Recession. Market-wide average and median prices based on reported sales activity appreciated. Those increases resulted from prices in the smaller property market, which traditionally range higher than per-acre prices for large properties, composing a larger-than-normal percentage of all transactions.

That scenario emerged in Texas in 2009 in the wake of the Great Recession. Market-wide average and median prices based on reported sales activity appreciated. Those increases resulted from prices in the smaller property market, which traditionally range higher than per-acre prices for large properties, composing a larger-than-normal percentage of all transactions.

This report analyzes land markets segmented by size for six of Texas’ seven land regions. Using the acreage distribution of sales reported to the Real Estate Center from 1966 through 2009, the Center estimated the quintiles of size of transaction over a period that had varying socio-economic conditions. Quintiles divide a population into fifths. Specifically, the 20th percentile represents the size where 20 percent of the population of sales are equal to or smaller than that acreage value. Quintiles are defined by the 20th, 40th, 60th, and 80th percentile.

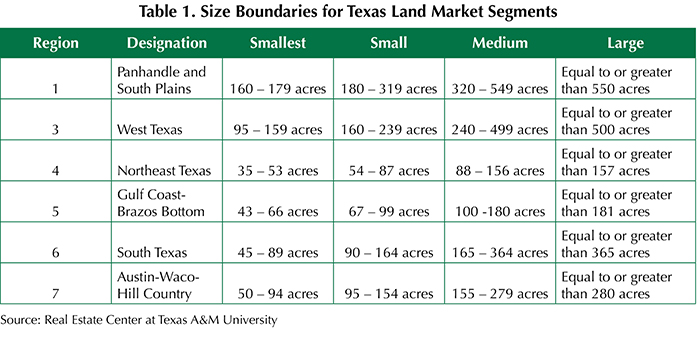

The first quintile represents a separate market with its own dynamics. It is analyzed separately and not reported here. The Center’s study of rural land markets concentrated on the next four quintiles beginning with sales of properties with a size ranked between the 20th and 40th percentile in each region of Texas. This is the smallest-sized market segment. Each quintile value served as a guide in setting the boundaries of the market segments. This process produced four market segments for each region studied: smallest, small, medium, and large. The distributions varied by region, resulting in a unique set of segment boundaries in each region (Tables 1 and 2). The Panhandle and South Plains and West Texas markets produced larger transactions in each segment than the remainder of the state.

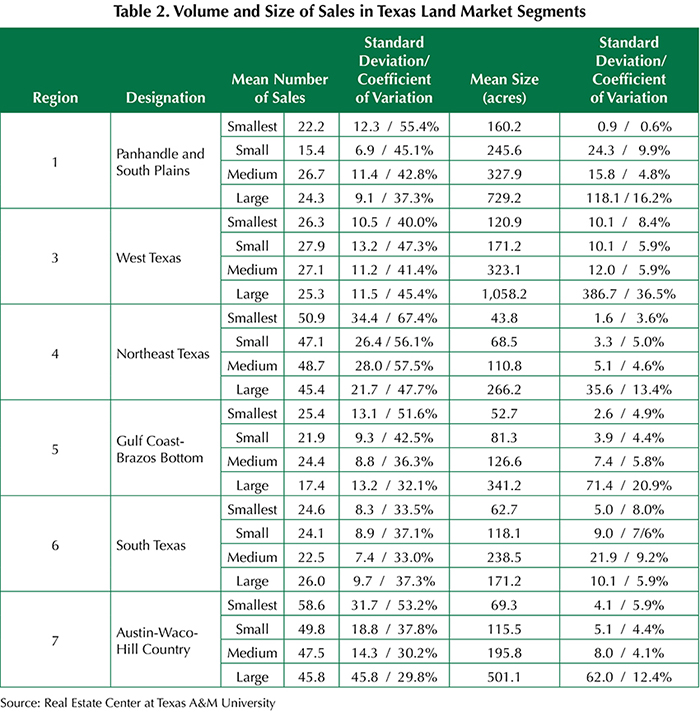

The smallest market segment for the Panhandle and South Plains registers an average of 22.2 transactions each year with a standard deviation of 12.3 for a coefficient of variation of 55.4 percent (Table 2). The average transaction consisted of 160.2 acres with a tiny standard deviation of 0.9 and a coefficient of variation of 0.6 percent.

In each region, the annual calculated median price and size for individual market segments indicate the typical per-acre price and size of transaction in the area. In addition, the analysis provided the number of sales and total acreage for transactions in each market segment. Using these statistics allowed calculation of real (inflation-adjusted) prices in 2019 dollars as well as the total dollar volume of transactions in each segment.

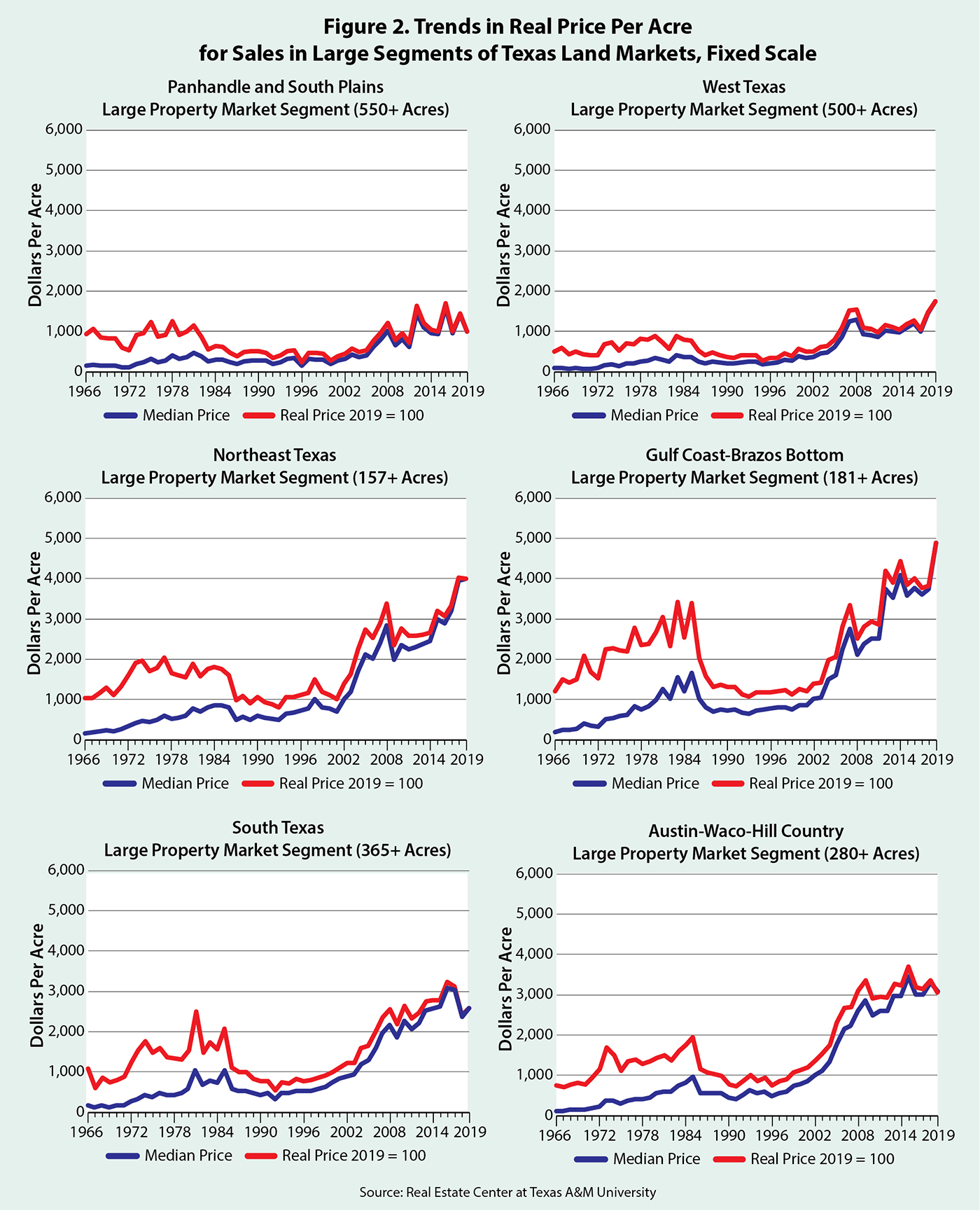

Figures 1 and 2 show price trends for sales in the large market segment for all of the regions studied. Figure 1 shows price trends across regions with variable scales on the vertical axis. This permits the greatest variability for the trend lines in each region. The blue lines in each figure represent the median price paid for land in the specified region for large properties. The orange lines present the median price adjusted to 2019 dollars. Figure 2 contains the same information set against a consistent scale in all regions with a maximum value of $6,000 per acre. The relative elevations in Figure 2 reflect the relationship between prices in large tract markets across Texas.

Large tract prices remained relatively steady in real terms from 1966 until the ’80s, when they experienced a pronounced decline (Figure 1). Real prices then settled into a narrow range followed by a rapid increase after 2000. From the 1970s through 1985, real prices remained relatively flat in all regions except the Gulf Coast-Brazos Bottom. Prices there rose consistently in real terms from 1966 through 1985. Otherwise, the regional large segment markets exhibited similar trends throughout the decades.

Figure 2 highlights the differences between price levels in the various regions. Reflecting the demographic realities of Texas, the Panhandle and South Plains and West Texas regions fall short of prices in the more populous Northeast Texas, Gulf Coast-Brazos Bottom, and Austin-Waco-Hill Country regions. In addition, those more densely populated regions saw more price growth than the former regions.

Median price multiplied by total acreage for each region in the large segment of the market produces an estimated real total dollar volume measured in 2019 dollars (Figure 3). Most regions fluctuated between $20 million and $40 million much of the time. However, at least four of the six regions exhibited a huge spike in volume in 2004, about the time investment funds began to target real estate. Additionally, the Panhandle and South Plains saw a remarkable one-year explosion in 1972, following the so-called Nixon shock in August 1971 and at the time of the Russian wheat deal in the summer of 1972. Apparently, investment money poured into the region’s agricultural land as rising prices caused an increase in total dollars involved in transactions. Total dollars invested in large land tracks exploded in the Northeast Texas, Austin-Waco-Hill Country, and Gulf Coast-Brazos Bottom regions in the five years after the Great Recession.

Figures 4 – 9 present similar analyses for the remaining market segments.

Except for the Panhandle region, price per acre and total dollars invested in all size categories of the land market exhibited significant increases since the Great Recession, reflecting the state’s general economic prosperity.

_______________

Dr. Gilliland ([email protected]) is a research economist and Su and Greaves are research interns with the Real Estate Center at Texas A&M University.

You might also like

TG Magazine

Check out the latest issue of our flagship publication.